The Production Linked Incentive (PLI) 2.0 scheme, backed by ₹17,000 crores in direct incentives for IT hardware manufacturing, is reshaping which components Indian procurement teams will source domestically by 2030. The parallel ₹76,000-crore Semicon India Programme is attracting foundry investment, wafer fabs, and assembly capacity. But the hardware stack is not monolithic. Understanding which three layers will become structurally Indian, which will not, and what that means for procurement is the real task.

PLI 2.0 and the Three-Layer Hardware Stack

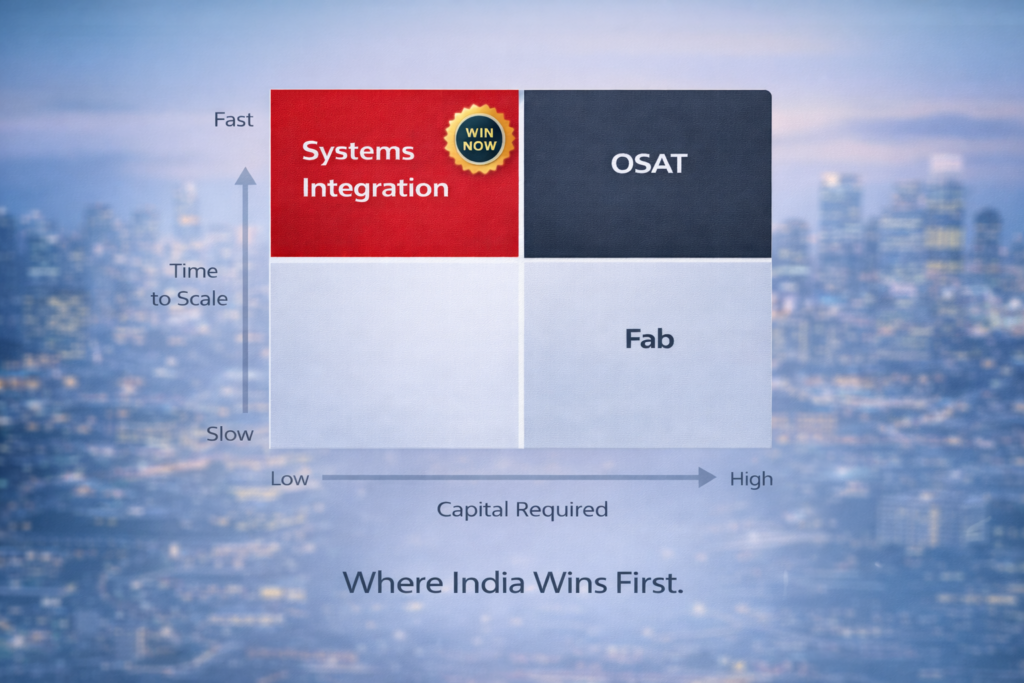

The IT hardware supply chain consists of three economic layers: silicon fabrication (fabs), component assembly and packaging (OSAT), and systems-level integration. Each has different capital requirements, technological complexity, and geopolitical constraints. PLI 2.0 targets the latter two layers deliberately.

Fabrication at leading-edge nodes (5nm and below) remains capital-intensive, requiring ₹10,000+ crores per fab and multi-year ramp cycles. India does not have a commercial 5nm fab today, and MeitY-backed capacity is still 5–10 years away even with Semicon India subsidies. The second layer, assembly, test, and packaging (OSAT), is where India wins first. Companies like Kaynes Electronics and CG Power have received PLI approval, with initial focus on notebook assembly, desktop systems, and peripheral components. The third layer, systems integration and motherboard design, is already maturing in India; firms like RDP and competitors are expanding here under PLI support. Procurement buyers should expect substantial domestic sourcing in OSAT and systems assembly by 2027–2028, while leading-edge silicon remains a global acquisition until at least 2031–2032.

Why Semicon India and PLI 2.0 Work in Parallel

The Semicon India Programme funds fabs, packaging units, and compound semiconductor capacity across multiple states. Micron Technologies’ announcement of a wafer fab in Sanand, Gujarat (capacitive DRAM and NAND), and the proposed Tata-PSMC foundry project in Tamil Nadu signal genuine capital mobilisation. Yet these assets serve different timelines and markets than PLI 2.0 procurement targets.

Semicon India addresses structural supply-chain vulnerability in memory and sub-leading-edge logic—commodities where India can compete on labour, land, and fiscal incentive. PLI 2.0, by contrast, targets the IT equipment OEM layer directly: it subsidises margins on notebooks, desktops, and systems sold domestically or exported from India. A buyer purchasing a PLI-eligible notebook in 2027 will benefit from Semicon India indirectly only if domestic packaging capacity supports that assembly. Until 2029–2030, the critical inputs—processors, GPUs, memory controllers—will still come from Taiwan, South Korea, and the USA. What changes is the cost of integration and the security of assembly supply.

The Real Procurement Decision: Custody vs. Cost

For CIOs and PSU IT heads, the key question is not whether to buy Indian, but what “Indian” means operationally. A PLI-eligible laptop assembled in Bangalore from Taiwanese memory and an imported Intel processor is more secure in supply continuity than an identical unit assembled in Taiwan. It is not sovereign in silicon, but it is sovereign in logistics and labour. The PLI mechanism subsidises the assembly margin by up to 3–4 per cent for enterprises meeting localisation thresholds on motherboards, keyboards, and chassis. For bulk procurement (10,000+ units), this subsidy compounds.

State IT secretaries should view Semicon India and PLI 2.0 through the lens of backward integration, not self-sufficiency. A wafer fab in Gujarat produces memory or sub-6nm logic that feeds assembly plants in Bangalore, Pune, and Hyderabad. Those plants then feed the OEM procurement market. The timeline is five years. By 2031, a significant share of memory and mature-node logic used in Indian IT hardware will be manufactured within India or South Asia. That is the structural shift. Until then, procurement decisions should weight supply-chain resilience, not pure localisation.

OSAT and Systems Integration: The Near-Term Winner

Assembly, test, and packaging is where India captures value and volume immediately. Kaynes’ PLI approval for notebook and desktop systems assembly, and CG Power’s similar status, means that by Q4 2026, domestic OSAT capacity will handle 15–20 per cent of India’s IT hardware demand. By 2028, the figure could reach 40 per cent. This is not hypothetical: it is reflected in PLI disbursement timelines and capex announcements.

Systems integration—the layer that includes motherboards, power supplies, thermal management, and industrial design—is already Indian-capable. Companies like RDP have spent fourteen years building this competency; PLI formalises and incentivises it. A buyer specifying an Indian-integrated system (with a Taiwanese processor and South Korean memory) reduces supply-chain latency, supports domestic employment, and qualifies for PLI subsidies. This layer is the procurement win in the 2026–2030 window. It is also where technical quality and intellectual property accrue to Indian firms.

MeitY’s Role: Standards, Not Subsidy Alone

While DPIIT and the Ministry of Commerce administer PLI and Semicon India, MeitY’s role is architectural. Government-IT procurement is now linked to MeitY compliance standards and Indian Standards Bureau (BIS) certification, which favour domestic suppliers. Additionally, MeitY’s Digital Infrastructure for Knowledge Economy (DIKE) initiative includes preferences for hardware sourced from PLI-eligible manufacturers in tenders over ₹1 crore. This creates a dual mechanism: PLI subsidises margins for OEMs, and government procurement de-risks volume for them. For buyers in the government ecosystem, this alignment is material.

State governments are following the same pattern. Several state IT departments have already signaled preference for PLI-eligible systems for classroom initiatives and office rollouts. Coupled with the Make in India directive, this creates a five-year moat for domestic OSAT and systems integrators. The subsidy matters, but the procurement preference matters more.

What Does This Mean for Buyers Between 2026 and 2030?

The answer depends on your institution and risk profile. If you are a PSU or government agency, sourcing from PLI-eligible manufacturers is now aligned with compliance and fiscal policy. You will likely see price competitiveness emerge as OSAT margins normalise after 2028. If you are a large enterprise, the choice is between global supply chains (mature, proven, but geopolitically exposed) and Indian-integrated chains (improving rapidly, cheaper in assembly, but dependent on imported silicon until 2031). A hybrid approach—strategic procurement from PLI-eligible systems integrators for 30–50 per cent of volume, with global diversification for the remainder—is prudent through 2028.

The semiconductor stack will not be Indian in five years. The systems stack will be. Procurement decisions should reflect this distinction. Buyers who understand the difference between substrate sovereignty and component sovereignty will navigate the 2026–2030 window more effectively than those betting on wholesale localisation. PLI 2.0 and Semicon India are shifting hardware procurement incentives, not reversing global supply chains.

For organisations looking to align procurement strategy with India’s semiconductor and systems roadmap, the opportunity is in OSAT and systems integration capacity, not in waiting for leading-edge fabs. The fiscal tail (PLI) will follow the structural head (OSAT and systems maturity). Procurement teams that build relationships with PLI-approved integrators and assemblers before 2027 will capture the value of scale and subsidy in the 2028–2030 window.

Table: India IT Hardware Policy Stack (2024–2030) — Launch, Allocation, and OEM Impact

| Policy / Scheme | Launch / Revision Year | Budget / Allocation | Primary Objective | Impact on Indian OEMs |

|---|---|---|---|---|

| PLI Scheme — IT Hardware (Phase 2) | 2023 (revised) | ₹17,000 cr over 6 years | Incentivise domestic production of laptops, tablets, servers, PCs | Direct revenue incentive (4–2% of incremental sales); drives local manufacturing scale-up |

| Semicon India Programme | 2022 (ongoing to 2030) | ₹76,000 cr | Build semiconductor design and fabrication ecosystem in India | Reduces long-term chip import dependency; enables indigenisation of compute components |

| IndiaAI Mission | 2024 | ₹10,372 cr (5 years) | Sovereign AI compute, datasets, and skilling infrastructure | Creates demand for Indian-assembled GPU servers and AI PCs in public sector |

| Trusted Sources List (MeitY) | 2023 (rolling updates) | No direct allocation; regulatory instrument | Restrict government procurement to supply-chain-verified hardware vendors | Compliance barrier to entry; advantage for Indian OEMs with auditable local supply chains |

| BIS Mandatory Certification (CRS expansion) | 2024 (expanded product scope) | No direct allocation; regulatory instrument | Quality and safety assurance for all electronics sold in India | Levels playing field; raises compliance cost for grey-market imports |

Related Reading

For the market-sizing that PLI 2.0 is unlocking, see India’s AI hardware market is about to triple — who wins. To discuss Make-in-India partnership opportunities, visit rdp.in/contact.